Accounting considerations for Payroll Protection Program (PPP) loan forgiveness

12/18/2020

By Scott Klitsch Principal CLA Boise, Idaho Email T. 208.387.6440

Many of you are familiar with the blog post we shared with you in April 2020 focused on the accounting considerations of processing and funding PPP loans. We wanted to update that post with a larger focus on the forgiveness process. Our summary of the primary accounting considerations financial institutions should consider, during the forgiveness phase of PPP loans, is included below.

|

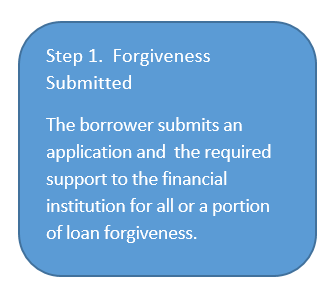

Accrue Interest Once the financial institution has obtained appropriate documentation from the borrower, they will analyze within the required timeframes and, in turn, submit their decision on forgiveness to the SBA and wait on the SBA’s decision on forgiveness. Interest continues to accrue during this time. |

|

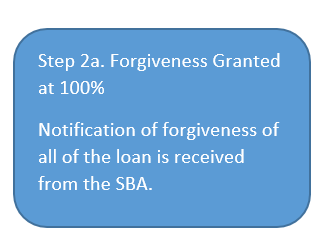

Remove loan and record cash receipt. Accelerate recognition of net deferred fees. Stop accrual of interest. The loan should continue to be accounted for as loan, including accrual of interest and amortization of net loan origination fees through the receipt of payment from the borrower or the SBA. Payments received from the borrower or the SBA prior to maturity of the loan are considered prepayments of the loan. The SBA remits the full forgiveness amount to the lender, plus any interest accrued through the date of payment. The institution will then communicate that the loan was forgiven to the borrower. In addition, accelerated recognition of deferred net loan fees will occur at the time the payment is received from the SBA. Similar to a prepayment, accrual of interest on the loan should stop on the date payment is received from the SBA. |

|

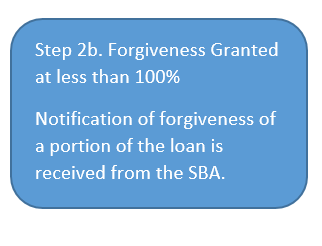

Remove loan and record cash receipt for portion of loan forgiven. Accelerate recognition of net deferred fees for portion of loan forgiven The loan should continue to be accounted for as loan, including accrual of interest and amortization of net loan origination fees through the receipt of payment from the borrower or the SBA. Payments received from the borrower or the SBA prior to maturity of the loan are considered prepayments of the loan. The SBA remits the appropriate forgiveness amount to the lender, plus any interest accrued through the date of payment. The institution will then communicate the forgiven amount to the borrower. In addition, accelerated recognition of deferred net loan fees will occur for the percentage of loan forgiven at the time the payment is received from the SBA. Similar to a prepayment, accrual of interest on the amount of the loan forgiven should stop on the date payment is received from the SBA. |

|

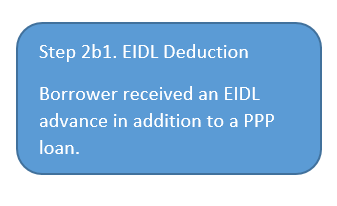

Service loan associated with EIDL advance If a borrower received an EIDL advance, the SBA is required to reduce the borrower’s PPP loan forgiveness amount by the amount of the EIDL advance. SBA will deduct the amount of the EIDL advance from the forgiveness amount remitted to the lender. Any remaining balance must be repaid by the borrower. The lender is responsible for notifying the borrower of the loan forgiveness amount remitted by the SBA and the date on which the borrower’s first loan payment is due and the lender must continue to service the loan. The borrower must repay the remaining loan balance and associated interest by the maturity date of the PPP loan. The lender will continue to amortize net deferred loan fees associated with the balance of the PPP loan that remains. |

|

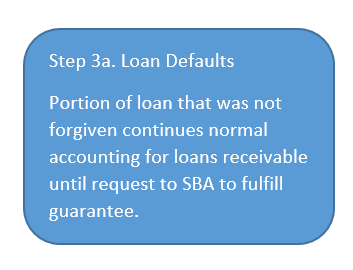

Record a receivable from SBA. Financial institutions will need to monitor loans throughout the remaining maturity term of the loan. If during either the ten-month deferral window of principal and interest or at any point in time afterwards, it becomes known that the non-forgiven portion of the loan will not or cannot be repaid by the borrower, the financial institution should seek performance under the guarantee from the SBA. The subsequent accounting would follow Step 2 above. |

|

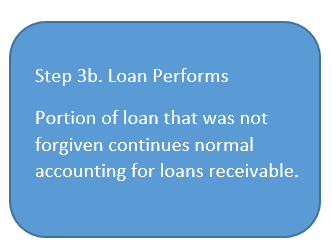

Record collection of principal and interest. The financial institution should continue to record accrual of interest and apply borrower payments like any other performing loan. |